New 401(k) Rules for 2026: High Earners Over 50 Must Use Roth for Catch-Up Contributions

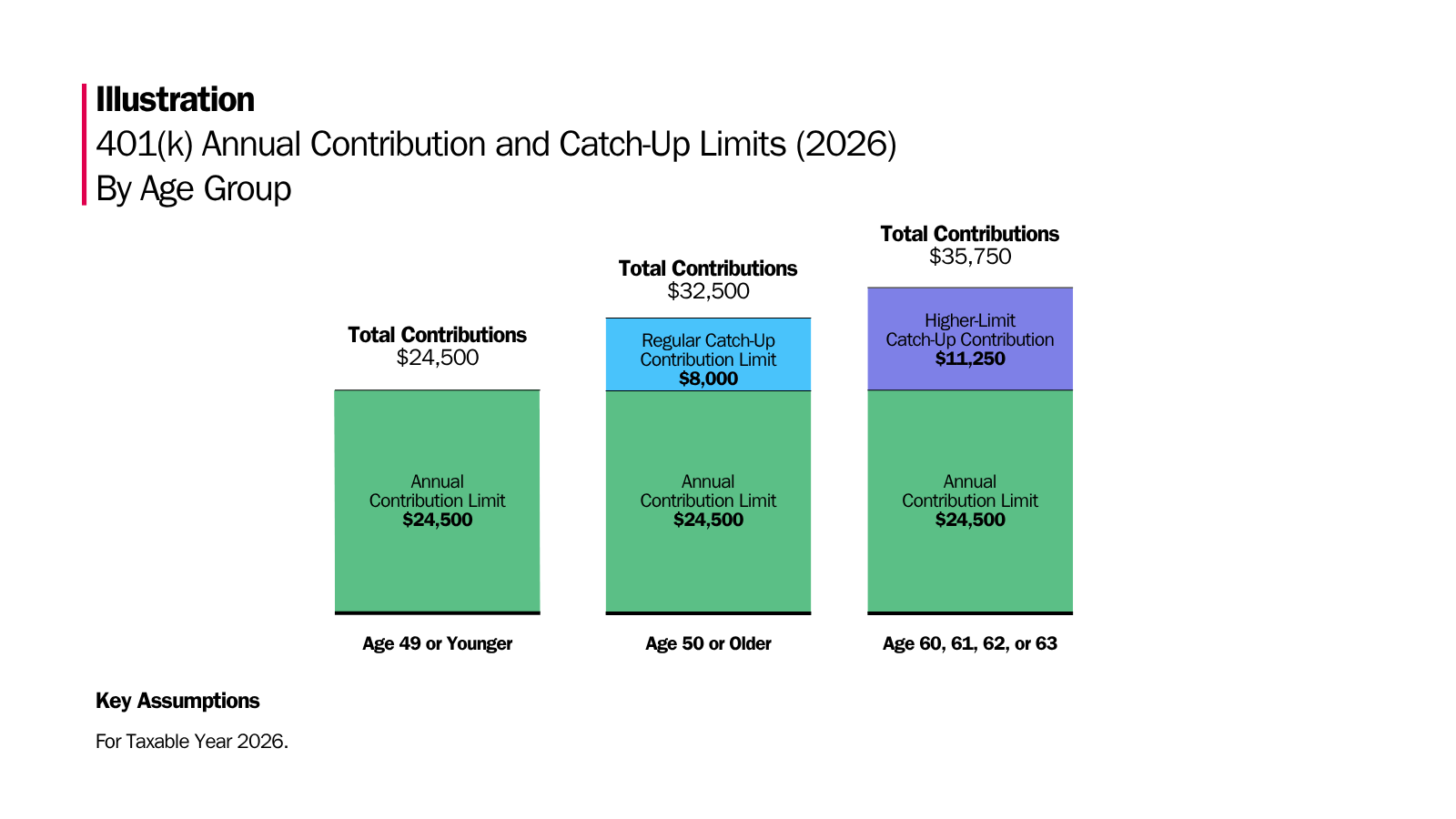

A new IRS rule took effect in 2026 requiring workers aged 50 and older who earned $150,000 or more in 2025 to make all catch-up contributions to their 401(k) on an after-tax Roth basis. The standard employee contribution limit also rose to $24,500, up from $23,500 in 2025. Workers aged 60 to 63 can contribute up to $11,250 in catch-up contributions under a new super catch-up provision.

A significant change to 401(k) rules took effect in 2026, requiring high-income workers aged 50 and older to direct all catch-up contributions into a Roth account rather than a traditional pre-tax plan.

The rule applies to employees who earned $150,000 or more in wages subject to FICA taxes in 2025. For those workers, catch-up contributions must be made on an after-tax basis. If their employer's plan does not offer a Roth option, they cannot make catch-up contributions at all in 2026.

The standard employee contribution limit for 401(k), 403(b), governmental 457 plans, and the federal Thrift Savings Plan rose to $24,500 for 2026, up from $23,500 in 2025. The combined limit for employee and employer contributions is $72,000.

Workers aged 50 and older who are not subject to the Roth mandate can still make standard catch-up contributions of $8,000. Workers aged 60 to 63 are eligible for a "super catch-up" of $11,250 under a provision introduced by the Secure 2.0 Act, provided their plan allows it.

Financial advisers are warning clients to check whether their employer's plan offers a Roth option before assuming they can make catch-up contributions. Some smaller employers have not yet added Roth accounts to their plans.

Kiplinger also flagged a separate issue: some companies have paused or reduced discretionary 401(k) matching contributions as part of cost-cutting measures. Advisers say workers should monitor their contribution pacing to avoid front-loading savings early in the year and missing out on employer match dollars available later.

IRA contribution limits also rose in 2026, to $7,500 for most savers. The deadline to contribute to an IRA for the 2026 tax year is April 15, 2027.