Trump Accounts Launch July 4 With 1000 Dollar Federal Seed Deposit for Children

The federal government launched Trump Accounts on July 4, 2026, a new tax-advantaged savings program for children under 18. Children born between 2025 and 2028 receive a 1,000 dollar seed deposit from the U.S. Treasury. Families can contribute up to 5,000 dollars per year, with funds invested in low-cost U.S. equity index funds.

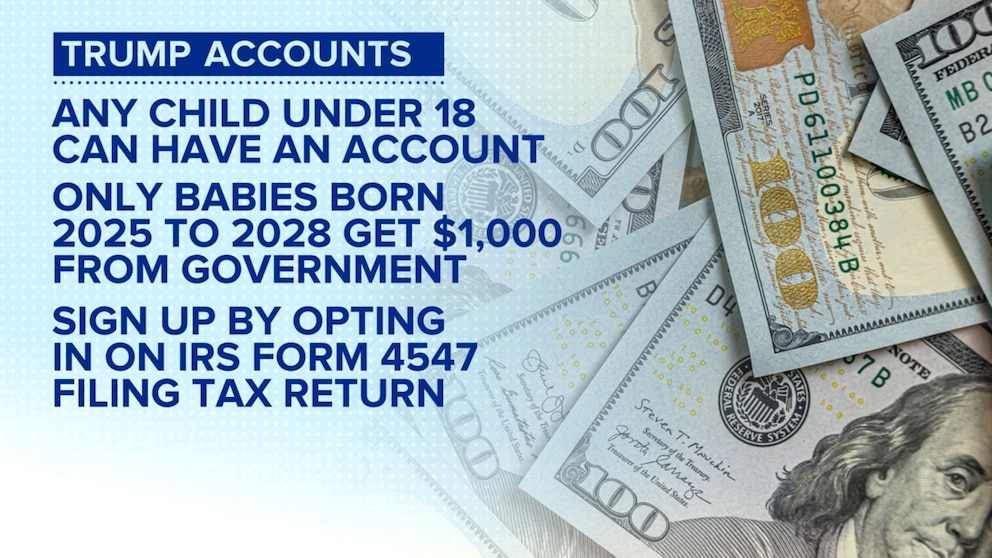

The federal government launched Trump Accounts on July 4, 2026, a new savings program for children under 18 established under the One Big Beautiful Bill Act. Children born between January 1, 2025, and December 31, 2028, receive a 1,000 dollar seed deposit from the U.S. Treasury.

Any U.S. citizen under 18 with a valid Social Security number is eligible. Accounts are opened by filing IRS Form 4547 or registering at TrumpAccounts.gov. Parents, guardians, and grandparents can open accounts on a child's behalf.

Families can contribute up to 5,000 dollars per year per child, with the cap indexed for inflation starting after 2027. Employers may contribute up to 2,500 dollars annually per employee through Section 125 cafeteria plans, counting toward the 5,000 dollar total. Contributions from state governments, tribal governments, or 501(c)(3) organizations do not count toward the annual limit.

During the growth period before the child turns 18, funds must be invested in low-cost U.S. equity index funds with annual fees capped at 0.1 percent. Leverage is prohibited. Earnings grow tax-deferred, and distributions are taxed as ordinary income. At age 18, the account converts to a standard traditional IRA.

Early withdrawals before age 59 and a half may trigger a 10 percent penalty, with exceptions for higher education expenses and first-time home purchases.

Unlike 529 plans, Trump Accounts are structured primarily as retirement vehicles. Financial advisors note the accounts will likely be treated as student assets for FAFSA purposes, which could affect eligibility for need-based financial aid.

The IRS confirmed that contributions to these accounts will not trigger gift tax reporting.